Uncovering The Forgotten Art Of Capital Allocation: What Every Business Owner Needs To Know

While capital may be a commodity and more accessible than ever, capital allocation is a skill that seems to elude even the most experienced CEOs and entrepreneurs.

Soo much so that ‘The Outsiders’ (the best capital allocation book I’ve read), a book about eight ‘unconventional’ CEOs and their radically rational blueprint for capital allocation, is now a best selling book. It’s even received high praise from master capital allocators Warren Buffett and Charlie T Munger.

On the face of it, these ‘eight unconventional CEOs‘ didn’t do anything out of the ordinary. They used common-sense and napkin math to make financial decisions a 14-year-old kid could understand.

Yet these CEO’s and the companies they operated outperformed, their peers and competitors over long periods by amounts that are hard to believe.

According to Investopedia, “Capital allocation is about where and how a corporation’s chief executive officer (CEO) decides to spend the money that the company has earned. Capital allocation means distributing and investing a company’s financial resources in ways that will increase its efficiency and maximise its profits.”

In passing conversations I’ve had with business owners, capital allocation is rarely mentioned. It’s often an afterthought spotted with hindsight. Rather than a key contributor to business decision making.

A recent report published by the MBIE backs up my experience. Business owners state their biggest issues are:

1. Cash Flow issues

2. Planning

3. Sales & Marketing

A possible underlying cause and solution here is proper capital allocation.

You could view running a business as playing a game of Tetris. Each block or shape represents a resource that needs to be allocated in the business. When all the shapes are well-matched, i.e. resources have been allocated effectively, the business will score highly and perform well.

When the shapes are mismatched, i.e. resources haven’t been allocated effectively, the business will run inefficiently, score poorly, and cash flow will suffer.

For example. I once brought a business that was spending $7k per year on ‘nightlife’, a commercial music vendor that lets you display music videos on a screen for entertainment and $15k per year on radio advertising.

When I took ownership, I cut both of those activities. I replaced Nightlife with Spotify and radio advertising with google advertising.

Spotify saved the gym ~$6500 per year, and google ads saved the gym $10k per year. Customers liked the ‘new’ music, and google ads outperformed radio advertising.

We saved $10,500, improved our customer experience, and increased our customer leads. I took some mismatched shapes and refitted them.

Good Capital Allocation Outperforms Good Management

Jack Welch, a self and media acclaimed business guru, was General Electric’s CEO for 20 years. During those 20 years, the business performed ‘relatively’ well, and their stock price outperformed the S&P 500 index by some margin.

Jack now spends his time teaching businesses management theory and the general electric way. Making a handsome amount in the process.

In comparison, though, to the previously mentioned unconventional eight, general electrics performance was poor. None of those CEO’s wrote business books and received little media recognition. Yet, over the same period, they outperformed general electric by 600%.

‘A $10,000 investment with each of these CEOs, on average, would have been worth over $1.5 million twenty-five years later.’ – Fishpond.

On rare occasions when those CEO’s have been interviewed or shared their views on business, they don’t talk about management; they see that as a given of running a business. In summation, ‘putting the right people in the right jobs and paying them above-market rates to do said job if they did it well. Instead, they like to point to effective capital allocation as their key to success.

You might think, well, what do CEO’s of large corporations and capital allocation have to do with me and my business?

Here are two reasons you should care:

1. Increased cash flow to fund your lifestyle

2. Increased cash flow to reinvest in your business for future growth

It’s a dry and dull subject, but the rewards of doing it well are exciting.

Before we get to the how I’ll quickly touch on a few mental hurdles those unconventional eight managed to cross that allowed them to do their job (capital allocation) well.

They made decisions based on the objective success of their business. This one has tripped me up more than a few times. Many of us make decisions based on what makes us look good rather than what is best for our business. Ego boosting is an expensive hobby.

A few ways I’ve pissed money down the drain here

1. Signwriting vehicles

2. Business-class travel

3. Renting an office

4. Printing ‘business cards

5. Sponsoring events’

They didn’t care about or copy their competitors. They weren’t concerned with the Joneses.

Their competitors were flying around in corporate jets and spending all their days in meetings and playing golf. While these CEOs were sitting in their offices, reading, thinking and planning.

You won’t beat your competitors by becoming them.

They paid themselves last.

Warren Buffet has famously never paid himself more than $100k per year.

His reward is the increasing share price of Berkshire Hathaway. We have the same incentive; as the owners of our businesses, our net-worth increases when the value of our business increases.

Compounding returns. I might be flogging a dead horse here, but I’ll mention it anyway.

The Investopedia definition is ‘The compound return is the rate of return, usually expressed as a percentage, that represents the cumulative effect that a series of gains or losses has on an original amount of capital over a period of time.’

For example, you could invest $10k into a decently performing index fund, and on a good day, you might earn 8% after tax. After ten years, your original investment would more than double to $21,589.25.

The percentage you earn is where the magic happens.

If you invested that same amount into your business, say at a 25% return, which should be achievable. After ten years, your investment would be worth $93,132.

Additionally, your $10k investment could be generating your business cash flow of $19k per annum. Close to the entire value of the index fund investment.

To illustrate the point, here’s a story from this writer’s designated king of capital allocation, Warren Buffett.

“We bought See’s for $25 million when its sales were $30 million, and pre-tax earnings were less than $5 million. The capital then required to conduct the business was $8 million. (Modest seasonal debt was also needed for a few months each year.) Consequently, the company was earning 60% pre-tax on invested capital.

Last year See’s sales were $383 million, and pre-tax profits were $82 million. The capital now required to run the business is $40 million. This means we have had to reinvest only $32 million since 1972 to handle the modest physical growth – and somewhat immodest financial growth – of the business.

In the meantime, pre-tax earnings have totalled $1.35 billion. All of that, except for the $32 million, has been sent to Berkshire. After paying corporate taxes on the profits, we have used the rest to buy other attractive businesses. Just as Adam and Eve kick-started an activity that led to six billion humans, See’s has given birth to multiple new streams of cash for us. (The biblical command to “be fruitful and multiply” is one we take seriously at Berkshire.).”

Now, onto the process.

A Simple Capital Allocation Process

Simple is best for me, which I hope translates to easy to follow for you. No advanced mathematics, computer skills or calculators are required here.

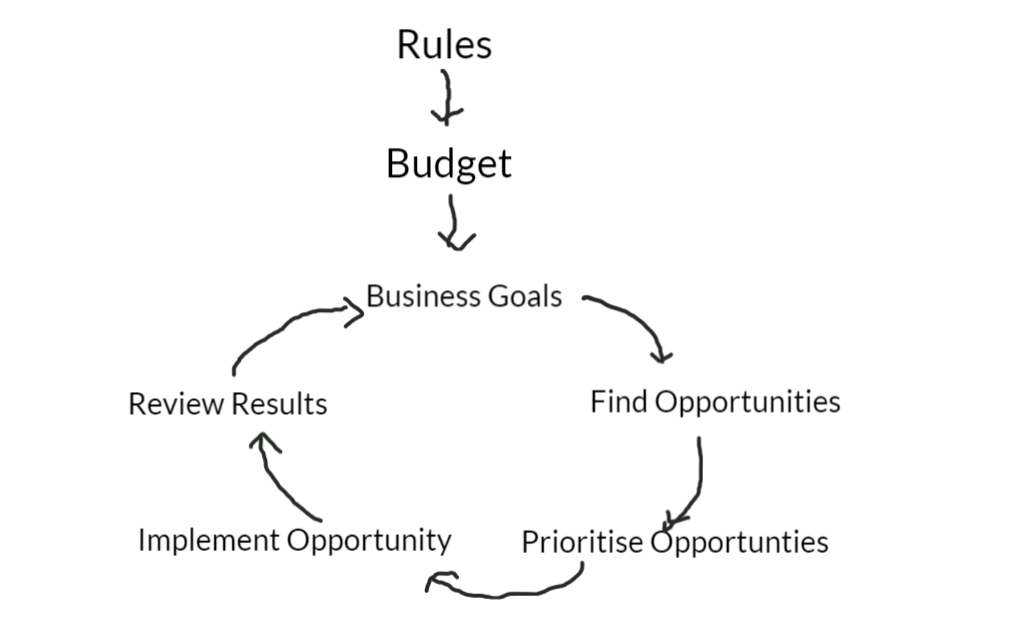

I use expectations, results and goals to create a flywheel that helps me continually allocate resources in my business in an increasingly effective manner.

My approach looks at investing in the existing operations of a business. Other forms of capital allocation like buying another company, paying down debt, or issuing dividends are areas I don’t have much experience in, so I won’t discuss that here.

I invest to improve cash flow rather than revenue or profits. ‘cash is king’ is the mantra.

INVESTMENT RULES

First, I set capital allocation rules.

These investing rules remove emotions from my decisions. They give me a heuristic to work with for future decisions. Most importantly, they filter out the rubbish and stop me from lazily working my way down a ‘todo’ list.

If my investments don’t produce the results, I expect I revise my ruleset. I let these rules determine my capital allocation performance rather than intuition or random data.

These rules will vary widely from business to business.

A venture-funded startup with massive opportunities in front of them can expect to earn significantly higher returns and take much higher risks than, say, an established small business with a small amount of cash on hand.

My gym, the vessel I’ll use to explain my capital allocation process here, is an established business (20+ years in operation) in a highly competitive market. Hence, we have fewer opportunities, less room to take risks and a lower expected return on said opportunities.

My rules for the gym are simple.

1. Any investment must have a payback period <12 months

2. Each investment must show promise of a compounding return

3. The total ROI on any investment must be >3x.

We use a payback period of 12 months because we are operating in a highly competitive and constantly changing market, and I want capital to be available in case we need to pivot. I can’t predict the environment we will be operating in for longer than 12 months soo any single investment could quickly become irrelevant beyond that period.

We require a compounding ROI because that’s how I view building a business, like laying bricks. Once one brick is applied, you can lay many on top, and that bottom brick will keep doing its job.

3X is our minimum long term return because I can quickly generate that from marketing activities; if we can’t invest in our business and earn a better return than I can from marketing, we’re better off investing that money into marketing.

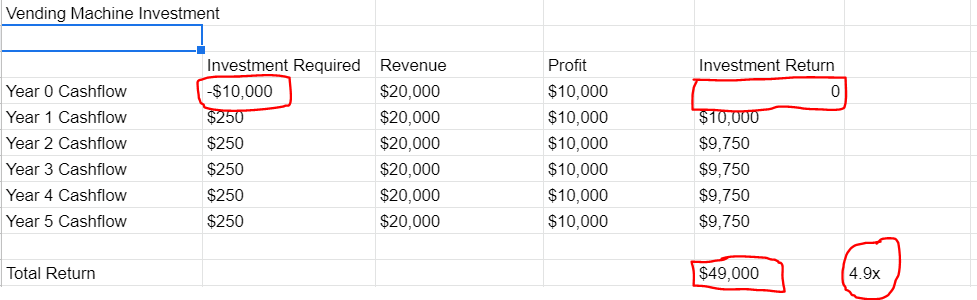

For example, At the moment, we’re looking at buying a vending machine to sell retail stock at reception like drinks and protein bars etc.

The cost of the machine is $10k. We need to be able to recoup that cost within a year. Given we can earn a 50% gross profit on product, we need to sell $20k of stock within 12 months to meet that rule. Based on past results, this is doable. – Tick.

The vending machine will continue to work and sell products for us for many years, so it will satisfy the compounding return rule. I.e. will continue to earn us money into the foreseeable future. – Tick.

Given the lifetime of a vending machine can be 10+ years, we expect the lifetime return of the machine to get close to 10x, far exceeding our 3x minimum return on investment. – Tick.

See numbers below.

CREATING A BUDGET

With my rules set, I need to know how much cash I have available to invest. So I create a budget.

- Without a budget, it’s really easy to get yourself into tax and other cash-flow related issues.

- Creating a budget is easier if you can afford to pay yourself a set amount each week rather than drawing cash at random.

My budgeting technique is basic. I take the average of the past 12 months and use those numbers to set my budget for January, which I call my base month. Then I forecast the rest of the year by adding in a growth factor based on business goals.

If your business is seasonal, you’ll want to take that into account as well.

I create and manage my budgets in a google sheet (see below). If you’re not comfortable doing this yourself, just ask your accountant to help.

As you can see, the primary revenue sources are membership revenue, trainer rent payments and retail sales. We’ve set growth goals for each revenue source that is factored into the budget above.

Fixed expenses remain the same throughout the year, and I set variable costs at a percentage of revenue based on the previous 12 months percentage.

For example, accounting is fixed at $220 per month. In contrast, Tribe wages continue to increase with revenue throughout the year.

Our year-end target is 500 members. You can see ‘paying members’ increasing each month and revenue + variable expenses rising with them.

• Mine and my business partners wages are, accounted for in the budget.

The second part of the budget is slightly more complicated.

There are four key components here.

Our ‘cash balance’, ‘profit’, ‘capital investments’ & ‘partner distributions’.

I like to keep a margin of safety in the business, and so over the year, I don’t like the cash balance of the business to drop below the equivalent of 3 months operating expenses.

Cash Balance = Money available in the kitty.

Profit = Cash inflows for the month

Capital Investments = Funds allocated for re-investment

Partner Distributions = Funds paid out to my business partner and me each month

We’ve set partner distributions at 40% of profit and cash allocated for investment at 7.5% of the money on hand.

In Summary

1. Use previous 12-month averages to set your base numbers for January

2. Use your business goals to project out the next 11 months

3. Identify and understand the difference between fixed and variable costs

4. Account for owners wages in the budget

5. Set a margin of safety cash balance based on monthly operating expenses

6. Calculate capital available for investment based on cash inflows, cash balance and future profits.

Month to month actuals vs budgeted numbers vary; however, over 12 months, I can predict how our business will perform with a high degree of accuracy.

If we start missing projected revenue and profit numbers and can’t get back on track, we’ll reset our budget.

In some cases, we’ll be able to adjust variable expenses.

For example, our wage costs start at $7,500 in Jan and increase to $20,400 by December. For that to happen, we need to hire more staff and increase pay rates. That’s not something we have to do but what we have the option to do as the business grows.

After completing our budget, I add up the total ‘capital investments for the year, which comes to $46,100. Now I know how much we have to invest.

I like to invest our capital funds as early in the year as possible and put it to work, which gives us the best chance to hit our business objectives.

I learned this lesson the hard way.

When I first purchased the gym, the business was losing an absurd amount of money ~$150k per annum (that’s a long story). I had $60k cash set aside to invest into the business, but because our outflows were so high, I was too scared to do anything with the money. Instead, that money sat in the business account and withered away to nothing. Then I had to take out another loan just to do what I should have done in the first place. I.e. Find opportunities to invest in the business with a good ROI and improve our chances of surviving.

The business was much better off by me putting that money to work even with high negative cash flow rather than leaving it sitting in the bank earning 1% per annum.

FINDING OPPORTUNITIES

Annually and quarterly, we review our business activities for the previous period. Based on successes, failures and a comparison to our business objectives, we create a business development plan for the next period.

Some might call this a business roadmap.

On this plan, I list all the opportunities we’ve identified during the previous business period and spend time with my business partner brainstorming with others.

(I’ll be writing about how I create a business roadmap and link that to this article here shortly.)

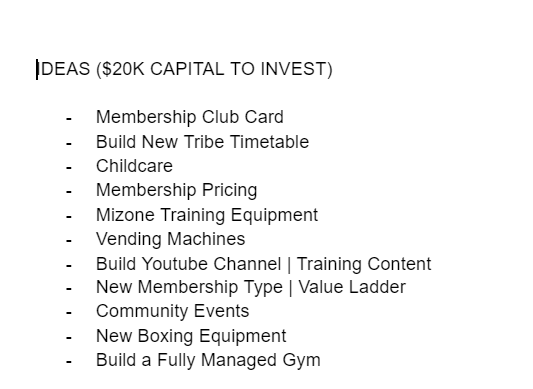

Below are the ideas we came up with for our Q1 2021 roadmap.

As you can see, these ‘opportunities’ aren’t restricted to investments in physical assets. Some are administrative like membership pricing, while others are marketing-related, e.g. ‘building a youtube channel’. Where cash isn’t required, I consider the value of mine or my team’s time it would take to capture that opportunity.

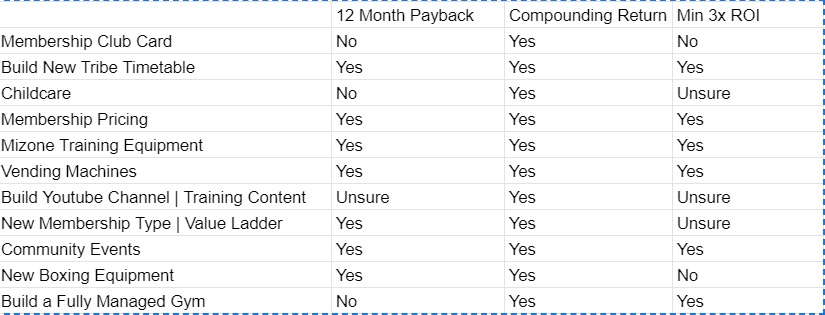

I take that list and run it through my filter (capital allocation rules) on a spreadsheet (like below).

I pick the opportunities that received a yes to all three requirements and investigate them further.

Some only need a rough PnL calculation to assess, like the vending machine example, while others require deductive reasoning to consider.

Take ‘community events, for example, a recurring item on our opportunities list.

The purpose of creating ‘community events’ is to keep our members engaged, help facilitate a connection between members and reduce our membership churn over time. We also encourage our members to bring friends and partners along, hopefully resulting in new membership sales.

The cost of each event is between $250 & $500, so over 12 months ~$5,000. If this helps us reduce our membership churn rate by one percentage point, we will retain ten extra members over a year, roughly valued at $10,000.

Reducing churn and new members is likely but not provable; even with hindsight, knowing exact numbers to run a PnL is impossible. Logically we think this is a probable outcome and one we’re willing to bet on.

The reality is people and business are far more complex than we’d like to believe, with possibly 1,000’s of variables contributing to an outcome. I guess the main point is, this is never an exact science or as simple as adding numbers. You’ve got to bet on your business sense as well.

PRIORITISE YOUR INVESTMENTS

As you’ll know, In business, virtually nothing goes to plan. For whatever reason, we decided to ignore prioritisation last quarter and paid the price for it.

We tried to act on all the opportunities we identified in Q1 that made it through our filter. In the end, we only half-completed two out of the five.

Working on too many things at once seldom works.

Lesson learnt = Choose your best opportunity and capture it first. Only move onto the next when the first is complete.

REVIEW INVESTMENT OUTCOMES

Starting our community events has had a negligible effect on churn to date and not generated us any new members. Hopefully, that will play out positively over the next 12 months.

These ‘failures’ are where we learn the most. The last and perhaps most important step in my capital allocation process is capturing and reviewing the results of my decisions.

I do this both intuitively and purposely.

Intuitively I will look for insights from our team, members and staff throughout the year that could indicate whether a particular opportunity has paid off or not.

At the end of each year and quarter, I review the different initiatives or opportunities we’ve acted on and try to understand if the outcomes have matched our expectations.

If they have been ‘successful’, was it for the reasons we thought?

If they haven’t been successful, then why? And what can we learn from that outcome?

As John Kavanagh likes to say, ‘Win or learn.’

The more times I’ve gone through this process, the better I’ve got at picking and the best opportunities and predicting their outcomes.

END RESULT

Over time the result of continuously effectively allocating resources will produce substantial positive results for any business.

Our gym, for instance, is a bit of a comeback story. Just 12 months ago, after coming out of our first lockdown for Covid, we lost 125 members and were losing up to $10k per month. Our business was virtually worthless.

After rigorously allocating our resources in the most effective way possible, we’ve just had a record month for revenue, profit and membership numbers. We’ve so far managed to meet our budget/projections, and with many good opportunities ahead of us, I’m excited to see how the rest of this year plays out.

I’m quietly confident we’ll be a $1 million business by the end of this year.

One comment

Pingbacks and Tracebacks

[…] How to make capital allocation decisions | […]